MEA data center colocation market shows strong growth driven by AI demand, hyperscaler expansion and hybrid cloud adoption. Key opportunities include sovereign AI investments in the Gulf, energy-efficient power in Africa and cooling technologies in the Middle East, with a focus on regulatory compliance and market entry by key players.

African and Middle Eastern Data Center Colocation Market

African and Middle Eastern Data Center Colocation Market ·GlobeNewswire Inc.

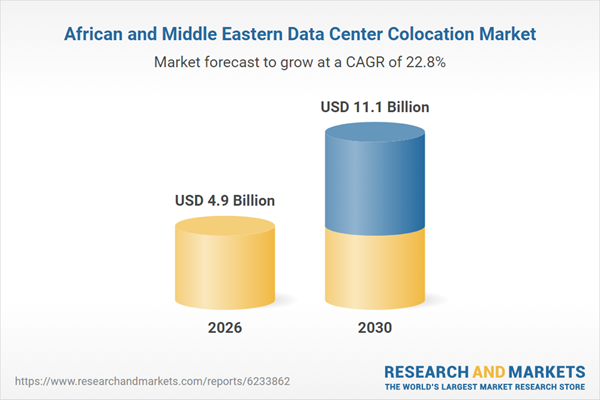

The Middle East and Africa data center colocation market is expected to grow by 28.5% on an annual basis to reach US$4.9 billion in 2026. The colocation market in the Middle East and Africa has demonstrated consistent expansion during 2021-2025, registering a CAGR of 24.7%. This growth pace is expected to accelerate during the forecast period, with the market projected to register 22.8% by 2026-2030. The colocation market is projected to grow from US$3.8 billion in 2025 to approximately US$11.1 billion by the end of 2030, driven by growing demand for AI and GPU workloads, accelerating hyperscaler capacity building, and continued enterprise adoption of hybrid multi-cloud infrastructure.

Africa's colo market is in the early stages of a structural growth phase driven by undersea cable investments, hyperscale market penetration and the fundamental development of African digital economies. South Africa's Johannesburg market is the continent's investment-grade anchor, while Kenya and Nigeria represent the next level of growth opportunity. The continent's universal challenge of power infrastructure is being addressed through increasingly sophisticated on-site generation solutions, and operators who master energy-autonomous data center operations in African conditions will have a sustainable competitive advantage. The regulatory landscape is rapidly maturing in many jurisdictions, and the Africa Colo opportunity rewards operators and investors with long investment horizons, infrastructure execution capabilities and genuine local market knowledge.

The Middle East colo market is undergoing a fundamental transformation, with Saudi Arabia's government-backed digital transformation investments transforming the region from UAE-dominant to a dual-market structure with significant secondary market growth in Qatar and Kuwait. Sovereign AI infrastructure investments and data localization mandates are creating a protected demand base that will sustain colo investments for the next decade. The UAE maintains its advantage in commercial connectivity density and established hyperscale ecosystem, while Saudi Arabia's scale of government commitment and capital availability makes it the fastest-growing market in the region. For operators and investors, the Middle East presents an attractive combination of government-secured demand, premium pricing for sovereign-compliant infrastructure, and a long investment runway driven by Vision 2030 and equivalent national transformation programmes, balanced against the operational demands of extreme climate conditions and the complexity of sovereign investment requirements.

competitive landscape

Current Market Situation: Africa's colo market is in its early stages globally but is growing rapidly from a small base. South Africa is the most developed African market, with Nigeria, Kenya and Egypt at the next level. The market is characterized by limited supply, growing demand and high infrastructure investment requirements driven by power and connectivity constraints. The Middle East colo market is led by the United Arab Emirates (Dubai and Abu Dhabi) and is growing rapidly in Saudi Arabia. Qatar, Kuwait and Bahrain have small but growing markets. The sector is characterized by government-aligned investment and commercial enterprise and hyperscale demand as well as sovereign-directed demand.

Major players and new players: Teraco Data Environments (South Africa): the continent's most carrier-intensive colo operator, Africa Data Centers (Liquid Intelligent Technologies): operates in South Africa, Nigeria, Kenya and other African markets, Vantage Data Centres: has entered South Africa with a major Johannesburg campus, Raxio Data Centres: operates in Uganda, Ethiopia, Mozambique and other East African markets, MainOne (acquired by Equinix): provides colo and connectivity in Nigeria and Ghana, WIOCC and Seacom: carrier-focused data center and connectivity infrastructure, Equinix, Khazanah (Mubadala), Gulf Data Hub, G42, e& (Etisalat), and du operate facilities in Dubai and Abu Dhabi, stc (Saudi Telecom Company), Datavolt, and Colt DCS leading colo in Riyadh Developing capabilities.

Recent launches, mergers and acquisitions

In Africa, Raxio has given the go-ahead to several East African facilities in 2025. Africa Data Center continues regional expansion. Vantage Data Centers advances the development of its Johannesburg campus.

In the Middle East, Datavolt and Colt DCS have advanced Riyadh data center development to 2025. Saudi Aramco has partnered with hyperscalers for cloud infrastructure in the Kingdom. UAE operators continue capacity expansion in Abu Dhabi and Dubai. G42 has signed cloud partnership agreements with several global technology companies.

Infrastructure and regulatory environment

Power grid access and energy mix

Africa's electricity infrastructure is hindering the continent's development. South Africa, Egypt, Morocco and Kenya have the most developed grids, but long-term reliability challenges most clearly affect South Africa's Eskom load shedding – all major African colo markets. Africa has substantial renewable energy potential: solar in the Sahel and Southern Africa, hydropower in Eastern and Central Africa, and wind in South Africa and Morocco. Falling solar and battery storage costs are enabling off-grid or hybrid colo power models. New large-scale renewable projects, including South Africa's REIPPPP auction and Kenyan geothermal developments, are adding clean energy capacity.

Middle Eastern electricity grids are generally reliable, with GCC countries having well-maintained infrastructure. The UAE's DEWA and Saudi Arabia's SEC provide relatively stable electricity. The region is investing in renewable energy – Saudi Arabia's NEOM and Vision 2030 include large-scale solar and wind development, and the UAE's Masdar is a global renewable energy developer, but current data center operations rely primarily on natural gas-based generation. GCC grid interconnection provides additional regional flexibility. The cost of cooling energy is high given the extreme ambient temperatures, making cooling efficiency a central operational variable for Middle East colo profitability.

Government policy and data localization

South Africa: POPIA: Africa's most mature data protection framework with region-specific localization requirements.

Kenya: Data Protection Act 2019: operational framework with ongoing regulatory developments.

Nigeria: Data Protection Act 2023: Enacted, with enforcement activity picking up.

African Union: Convention on Cybersecurity and Personal Data Protection: Continental Framework; Ratification varies by member state.

Saudi Arabia: Personal Data Protection Law (PDPL) and cloud computing regulatory framework: specified data categories must be hosted domestically; Foreign investment in critical digital infrastructure is subject to national security review.

United Arab Emirates: PDPL, ADGM, and DIFC frameworks: structured governance in onshore and financial free zone jurisdictions.

Queue: National Cyber Security Strategy: This includes data governance and domestic hosting requirements.

barriers to expansion

Africa: Reliability of power infrastructure is the primary constraint in most markets. Political and economic stability varies greatly between markets. Foreign exchange risk affects equipment purchases and financing. Legal and regulatory complexity varies by country. Talent for data center construction and operation is limited. Internet infrastructure is underdeveloped in many markets outside primary cities.

Middle East: Cooling costs in extreme heat are a universal operational challenge. Water scarcity limits water-based cooling options. Talent for specific data center roles is limited domestically and depends on international recruitment. Regulatory approval for foreign-operated infrastructure in Saudi Arabia can be complex. Despite declining construction costs, those for specialized data center facilities remain high.

A bundled offering consisting of the following 4 reports, containing 192 tables and 224 figures:

Middle East and Africa Data Center Colocation Market Size and Forecast (2021-2030) Databook

Saudi Arabia Data Center Colocation Market Size and Forecast (2021-2030) Databook

South Africa Data Center Colocation Market Size and Forecast (2021-2030) Databook

UAE Data Center Colocation Market Size and Forecast (2021-2030) Databook

leading strand:

Report Attribute

Description

number of pages

500

forecast period

2026 – 2030

Estimated market cap in 2026 (USD).

$4.9 billion

Estimated market value by 2030 (USD).

$11.1 billion

compound annual growth rate

22.8%

Area covered

Africa, Middle East

Report scope for each report

Data Center Market Overview

Total Data Center Market Revenue

Total Installed Electrical Capacity (MW)

Colocation Share in Total Data Center Market (%)

Data Center Colocation Market Size and Forecast

Colocation Market by Service Type

retail colocation

bulk colocation

Colocation Market by Facility Architecture

Colocation Market by Customer Segment

Artificial Intelligence Colocation Market

Non-Artificial Intelligence Colocation Market

Colocation Market by End-Use Sector

Information Technology and IT Enabled Services

Banking, Financial Services and Insurance

telecommunication

retail

Media, gaming and entertainment

Production

Government

Other

data center capacity pipeline

total operating capacity

total capacity under construction

Planned and declared capacity

data center operational efficiency metrics

Power Usage Effectiveness (PUE)

energy reuse factor

renewable energy factor

cooling system efficiency

Average Rack Power Density

Artificial Intelligence vs. Traditional Workload Density

About ResearchandMarkets.com ResearchandMarkets.com is the world's leading source for international market research reports and market data. We provide you with the latest data on international and regional markets, key industries, top companies, new products and latest trends.

Attachment

Contact: Contact: researchandmarkets.com Laura Wood, Senior Press Manager press@researhandmarkets.com Call 1-917-300-0470 for EST office hours, call 1-917-300-0470 for US/Toll Free call 1-800-526-8630 for GMT office hours +353-1-416-8900