The South Africa data center colocation market offers growth opportunities driven by AI demand, hyperscale growth and hybrid multi-cloud adoption. Johannesburg is leading as a regional center with the advantage of connectivity and financial sector. Challenges include power infrastructure constraints, highlighting the need for energy flexibility.

South African data center colocation market

South African data center colocation market ·GlobeNewswire Inc.

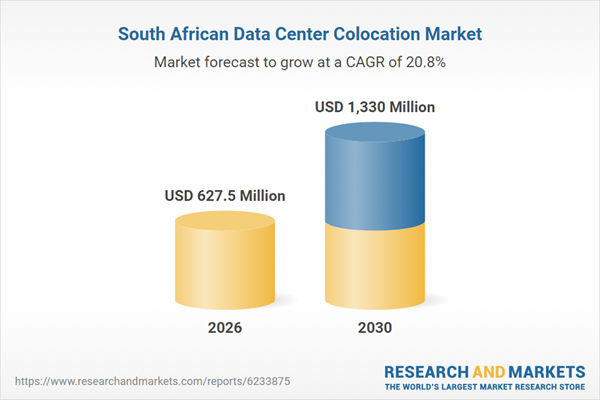

The South Africa data center colocation market is expected to grow by 26.5% on an annual basis to reach US$627.5 million in 2026. The colocation market in South Africa has demonstrated consistent expansion during 2021-2025, registering a CAGR of 23.1%.

This pace of growth has accelerated during the forecast period, with the market projected to register 20.8% by 2026-2030. By the end of 2030, the colocation market is projected to grow from US$496.0 million in 2025 to approximately US$1.33 billion, driven by increasing demand for AI and GPU workloads, accelerating hyperscaler capacity building, and continued enterprise adoption of hybrid multi-cloud infrastructure.

South Africa is the most developed colo market in Africa. Johannesburg has most of the capacity. The market is growing from a relatively small base with significant growth acceleration driven by hyperscale entry and enterprise cloud adoption. Teraco Data Environment is the largest and most carrier-intensive colo operator in South Africa, operating out of the Isando and Longlake campuses in Johannesburg. Africa Data Center (part of Liquid Intelligent Technologies) is expanding across South Africa and other African markets. Vantage Data Centers announces entry into the South African market with the development of its Johannesburg campus. NTT Global Data Center operates in South Africa.

In 2025, Vantage Data Centers advances construction of its Johannesburg campus. Africa Data Centers continues its South Africa expansion programme. Investment will continue in South Africa due to strong demand. New entrants will face competition from established operators with connectivity density advantages. Cape Town will attract increased investment related to undersea cable activity.

Key trends and growth drivers

Johannesburg consolidated as sub-Saharan Africa's primary colo hub

Johannesburg, particularly the Samarand and Midrand corridor in Gauteng, is the major colo market in sub-Saharan Africa. In 2025, operators including Teraco, Africa Data Centers and Vantage Data Centers are developing new capacity in this corridor. Johannesburg's location at the junction of major terrestrial fiber routes and its position as Africa's financial capital drives demand for financial services, enterprise and increasingly hyperscale tenants.

Johannesburg's established financial services sector, corporate headquarters concentration, and reliable connectivity to East and West African subsea cables via terrestrial networks make it the default choice for regional colo.

Johannesburg will retain its sub-Saharan leadership. Cape Town will develop as a worthwhile secondary market given its submarine cable access.

Hyperscale arrival validates South African market maturity

Microsoft Azure operates the South Africa cloud region (Johannesburg and Cape Town) and has continued capacity investments into 2025. AWS and Google have established South Africa regions, driving imminent wholesale colo demand. This hyperscale presence is the most significant demand validation event in the history of South African Colo.

Data sovereignty considerations, enterprise demand for low-latency regional cloud access, and South Africa's role as a proxy for broader sub-Saharan African enterprise demand are driving hyperscale investments.

As cloud adoption deepens in South Africa and Sub-Saharan Africa, hyperscale wholesale demand will continue to grow. Colo operators with capacity near hyperscale facilities will benefit from demand in the ecosystem.

Power infrastructure bottleneck remains the region's defining challenge

Eskom's ongoing load shedding, while at reduced stages relative to peak levels in 2022–2023, remains an important operational consideration for South African data centers in 2025. Operators maintain extensive diesel generator capacity and are investing in solar and battery storage to manage grid instability. Many large KOLO campuses have deployed on-site solar power generation with battery backup to reduce reliance on diesel.

South Africa's structural electricity supply shortfall has not been fully resolved despite government efforts to add independent power generating capacity. The transition to a more diversified power generation market continues but will take several years to fully address the supply gap.

Operators who invest in energy flexibility infrastructure (solar, batteries, hybrid systems) will differentiate on reliability. Power costs and complexity will remain above global comparable market levels.

Infrastructure and regulatory environment

Power grid access and energy mix

Eskom generates and transmits most of South Africa's electricity. The grid faces generation capacity shortages with load shedding risks by 2025. Independent power producers are adding solar and wind capacity under the REIPPP, but full grid stabilization is a multi-year process. Data center operators in South Africa invest heavily in backup power, and major operators have deployed on-site solar power generation with battery storage to achieve energy autonomy for extended periods.

Government policy and data localization

South Africa's Personal Information Protection Act (POPIA), which is fully effective from 2021 and enforced by the information regulator until 2025, regulates personal data protection. The South African government has proposed data localization requirements for some key data categories in draft policy documents, although comprehensive localization legislation is not implemented until 2025. Government digital transformation initiatives are driving public sector cloud and data infrastructure procurement.

barriers to expansion

Power grid reliability and cost of backup systems are the primary constraints. Skilled data center operations labor is limited. Land and construction costs have increased with development activity in Johannesburg. Political and economic uncertainty adds a risk premium to long-term investment decisions.

South Africa's colo market is at a critical stage, transforming from a predominantly domestic enterprise market to a regional sub-Saharan African hub supported by hyperscale investments from major global cloud providers. Johannesburg's carrier density, financial services ecosystem and established operator infrastructure give it a structural edge over competing African markets. The power infrastructure challenge, although managed through substantial operator investment in generation flexibility, remains the market's defining operational constraint and persistent competitive factor. Operators that have built reliable power infrastructure and secured hyperscale anchor tenants are well-positioned as the market deepens, while the emerging regulatory framework and potential future localization requirements under POPIA will increasingly shape how enterprise data governance considerations influence colo purchasing decisions.

About ResearchandMarkets.com ResearchandMarkets.com is the world's leading source for international market research reports and market data. We provide you with the latest data on international and regional markets, key industries, top companies, new products and latest trends.

Attachment

Contact: Contact: researchandmarkets.com Laura Wood, Senior Press Manager press@researhandmarkets.com Call 1-917-300-0470 for EST office hours, call 1-917-300-0470 for US/Toll Free call 1-800-526-8630 for GMT office hours +353-1-416-8900